Who Will Finally Become the "Nielsen" of FAST?

Why don't we have a 'Nielsen of FAST'? Because the industry is lying to itself. I break down the definitional crisis inflating FAST projections by billions, and analyze the three options—from Playout Vendors to a Buy-Side Mandate—that could finally solve the measurement puzzle.

I recently sat down with a senior leader at a FAST channel operator, one of the OGs, and our conversation kept circling back to a baffling reality for 2026: How do we still not have a "Nielsen of FAST"? Despite the massive viewer migration to free ad-supported streaming, the industry is still grading its own homework. Everyone has a dashboard, but nobody has a unified currency. The platforms won't share data, the OEMs are building walled gardens, and media buyers are drowning in fragmented spreadsheets.

But before we can even attempt to solve the measurement crisis, we have to address the elephant in the room: The industry is lying to itself about what it's actually measuring.

Short on time? Click the image below to flip through the 10-slide executive summary deck.

The Tower of Babel: Why We Can't Measure What We Can't Define

Before we can even consider having a Nielsen of FAST, we have to address the industry's multi-billion-dollar identity crisis. Right now, no one can even agree on how to define the acronym. To grab headlines, major analysts are artificially inflating the market by measuring completely different mountains.

Yes, this is the same crusade I’ve been waging since before going to Amazon MGM Studios. Why? Because those inside the industry define FAST often differently to those outside, and this is causing tremendous confusion.

You don't have to look hard to see this in action. Take a recent piece in Puck, noting that Evan Shapiro estimates combined "FAST platforms" will overtake Netflix’s share of connected TV time by this summer.

Here is the dirty secret behind that headline: That estimate relies on Nielsen's The Gauge, which tracks total app usage on a TV glass but does not separate a platform's linear channel viewing from its on-demand (AVOD) viewing. When analysts combine the viewership of Tubi, Pluto TV, and The Roku Channel and declare that "FAST is beating Netflix," they are heavily counting AVOD. As we know, 95% of Tubi's consumption is actually on-demand movies, not linear channels.

What makes this definitional chaos even more maddening is that the platforms themselves know the difference. If you look at Tubi's own published insights, or listen to Fox’s earnings calls, they explicitly classify their primary content delivery method as on-demand AVOD. In their annual The Stream reports, they distinctly carve out their "curated FAST offering" as a separate linear feature, noting it is watched by only a subset of their massive AVOD audience. Similarly, Roku's own advertising research explicitly separates ad buying strategies between "AVOD channels" and "FAST channels," treating them as distinct environments.

Want to take it another step? All media companies define FAST as linear channels for their licensing deals. AVOD as a term existed before FAST, so if you’re licensing something for free on-demand streaming, that’s an AVOD deal. Linear streaming? That’s a FAST deal. Doing it on Tubi or Roku? That’s a free streaming service.

Yet, when cartographers build their mega-charts, they ignore the platforms' own definitions, sweeping all that massive on-demand AVOD viewing into the linear FAST bucket. This failure to sing from the same industry hymn sheet—a major pet peeve among ad buyers—creates massive distortions. Nowhere is this more obvious than with analyst firms like TVREV, which made waves a few years ago by projecting FAST ad spend will hit an astonishing $33.8 billion by 2025. How? Because they define FAST as a business model (all free streaming), lumping true linear channels together with massive VOD libraries and the broader free internet.

From what I’ve been told from those in the know, that $34 billion figure caused chaos in boardrooms, as strategies were drawn up for FAST (linear) by execs assuming that the definition matched their internal industry one, and people anticipated a tremendous windfall.

Other major firms, like eMarketer, take a financial view. They forecast a ~$9.0B US market for 2025 by tracking public earnings, counting 100% of Tubi's ad revenue as “FAST." Essentially the TVREV forecast minus what else they threw in. However, if you strip out the VOD bloat and look purely at the unit economics of true linear FAST channels, our FASTMaster Intelligence model shows the actual 2025 US market size is close to $3 billion. I would say it could be worth $6 billion by 2028.

This definitional chaos creates a dangerous future gap. Analysts are projecting future FAST revenues that would mathematically require 24/7 sitcom reruns to command $33.00 CPMs—rates usually reserved for Primetime Network TV. It defies all market logic. And it is exactly why advertisers are so hesitant. They read headlines about a $33 billion premium ecosystem overtaking Netflix, but when they go to buy, they hit a fragmented, sub-$3 billion linear reality that lacks basic unified measurement.

What a lot of analysts mean when they say FAST, is not FAST. It is Free Streaming. Something I touched on in 2020 at Variety VIP+ as an issue the industry needed to address and something that, close to 6 years later, remains one.

The Shifting Goalposts: From Reach to Revenue

This lack of a unified demographic currency is reaching a boiling point because advertiser expectations are shifting. CTV is being forced to transition from a top-of-funnel premium branding channel to a bottom-of-funnel performance channel.

Advertisers no longer just want to know who watched the ad; they want to know if that viewer visited their website or bought their product. While major walled gardens (like Roku, Samsung, or Amazon) can offer this closed-loop attribution within their own ecosystems, doing it across the highly fragmented, syndicated world of FAST is nearly impossible. Premium content is no longer enough to win ad dollars; you need premium proof of performance.

In other words, FAST channels aimed at “the old grannies” as I said on stage once, will no longer cut the mustard even if they bring in large hours of viewing. If the viewing hours are not sellable, it doesn’t matter if a channel gets 1 million or 100. (It might matter if your internal strategy prizes any hours over profits, but that should hopefully be fading away in FAST.)

With that performance mandate in mind, who is actually capable of becoming the standard for FAST measurement? Let's look at the contenders.

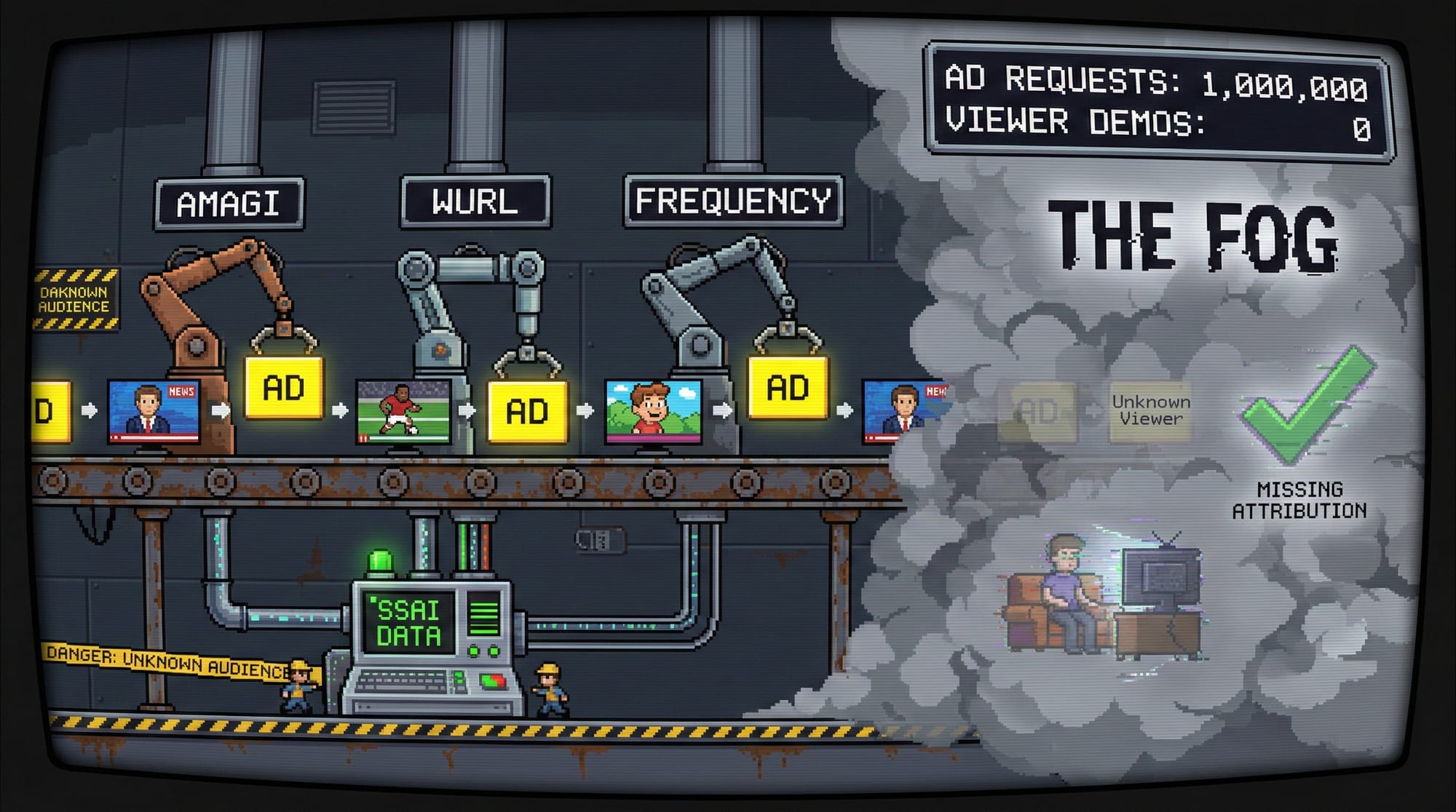

Option 1: The Playout Alliance

(The Infrastructure Play)

- The Concept: The major backend distributors—Amagi, Wurl, Frequency—pool their server-side ad insertion (SSAI) and routing data to create a unified viewership index.

- The Reality: They sit on the pipes. If they teamed up, they could theoretically create a unified viewership metric of all key syndicated channels, bypassing the walled gardens of the OEMs.

- The Roadblock: Playout vendors track streams and devices, not human demographics or downstream attribution. They see an ad request from an IP address, but they don't know if the viewer is a 45-year-old dad or a 14-year-old gamer. Furthermore, they are contractually restricted by content owners from weaponizing this data, and they would entirely miss the proprietary viewing on mega-apps like Tubi and Pluto.

- Probability of Becoming the Standard: 15%

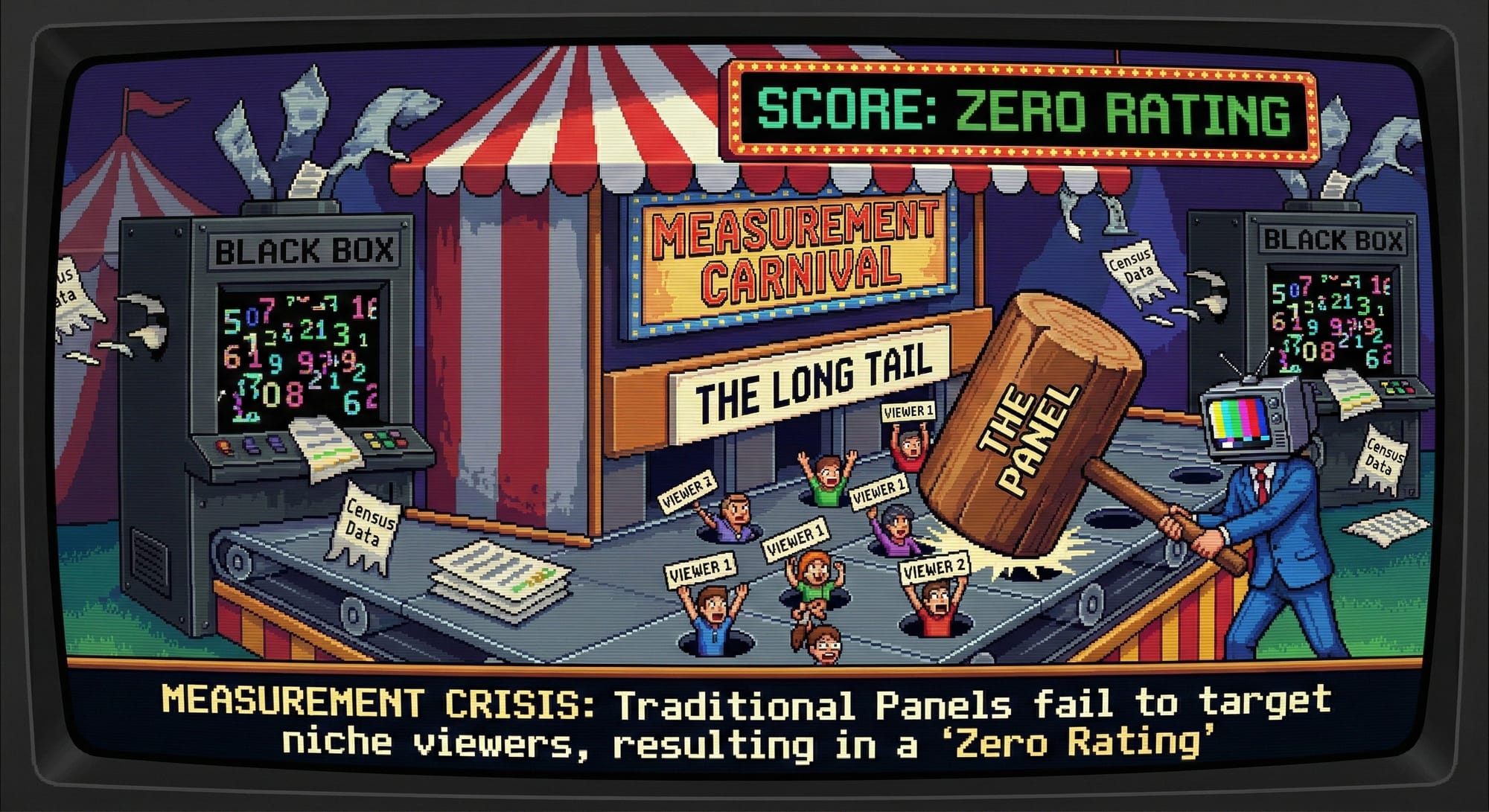

Option 2: The Traditional Titans Pivot

(Nielsen, VideoAmp, iSpot)

- The Concept: The legacy measurement companies finally figure out streaming by combining their traditional household panels with big data integrations to create a deduplicated FAST metric.

- The Reality: They have the historical trust of legacy ad buyers and the infrastructure to measure actual demographics.

- The Roadblock: Traditional panels mathematically fail at measuring the long tail of FAST. In a panel of 45,000 households, a niche FAST channel with 15,000 concurrent viewers will frequently register a literal zero rating simply because no panel member happened to be watching. Plus, getting the CTV platforms to hand over their proprietary census data so Nielsen can drop it into their heavily criticized algorithmic black box has been an endless, contentious game of cat-and-mouse.

- Probability of Becoming the Standard: 30%

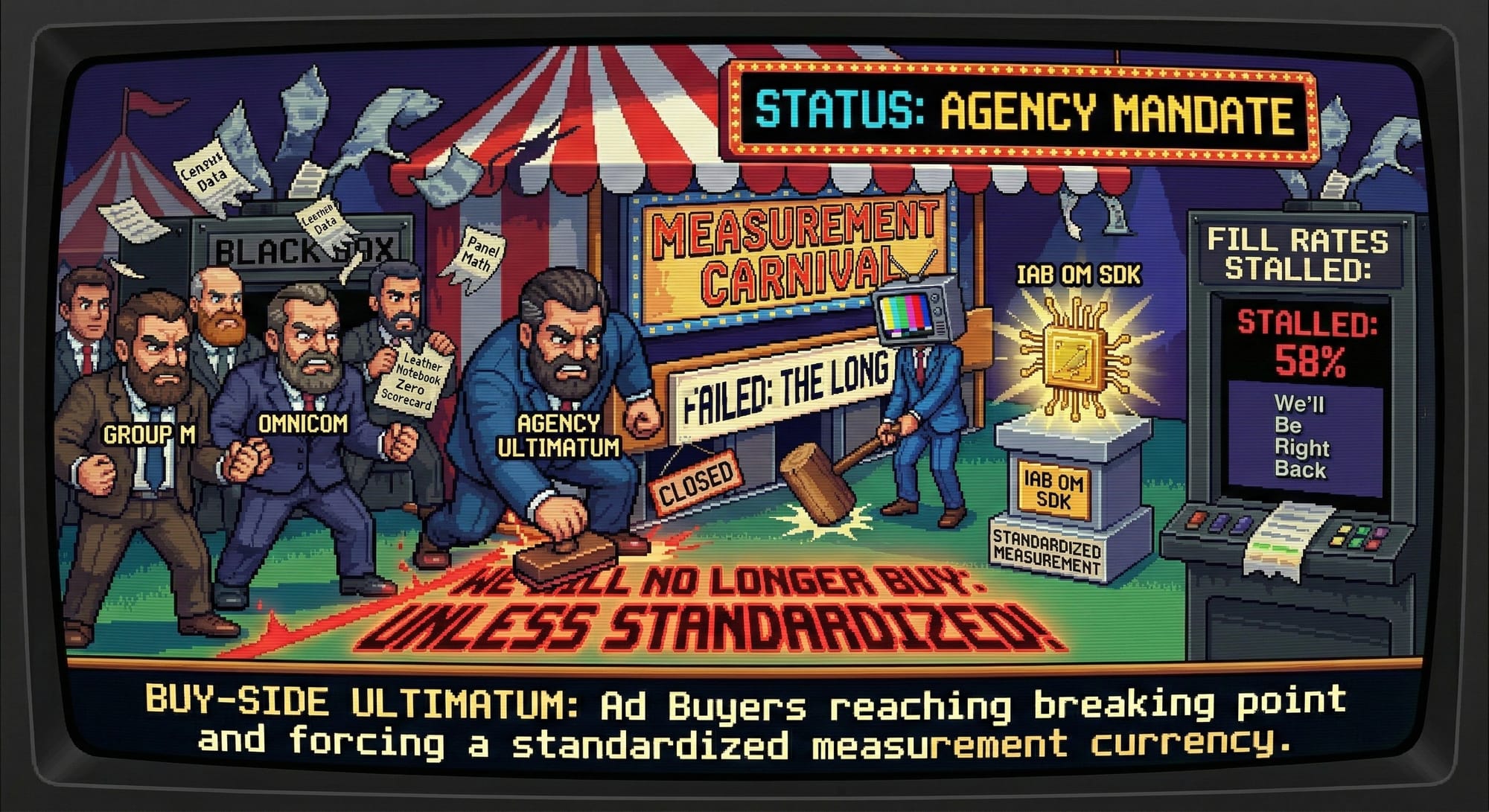

Option 3: The Buy-Side Ultimatum

(The Agency Mandate via IAB Tech Lab)

- The Concept: A massive holding company (like GroupM or Omnicom) gets fed up and draws a line in the sand: "We will no longer buy FAST inventory without third-party, standardized, deduplicated measurement."

- The Reality: This forces the industry to adopt a universal standard, likely driven by the IAB Tech Lab's Open Measurement SDK (OM SDK), which allows third-party measurement companies to seamlessly track ad delivery and performance across any platform without custom integrations.

- The Roadblock: Currently, buyers are treating FAST opportunistically. They tolerate the messy measurement because the CPMs are incredibly cheap ($10–$20 compared to premium CTV's $30+). However, this hesitation is one key reason why FAST suffers from notorious ad fill rate issues (the other being having hundreds of always-on channels that have low audience, creating an infinite number of ad breaks). Because advertisers won't commit premium, upfront dollars without trusted measurement and performance attribution, FAST channels frequently suffer from paid fill rates hovering between 50% and 65%, leaving viewers staring at repetitive in-house promos or "We'll Be Right Back" slates.

- Probability of Becoming the Standard: 45%

The Verdict

The "Nielsen of FAST" won't look like Nielsen at all. It won't be a single company releasing a weekly Top 10 list. Ultimately, the solution will be a framework born from advertiser frustration.

Until the industry agrees to sing from the same definitional hymn sheet, headline-grabbing forecasts will continue to distort the market. But to fix their dismal fill rates and prove the downstream performance buyers now demand, platforms will eventually be forced by agencies to adopt open standards and integrate into secure data clean rooms, where buyers can match their own first-party data against verifiable platform delivery.

Tired of grading your own homework?

If you need to navigate the measurement chaos, define your actual market size, or build an ad strategy that agencies will actually trust, you need an objective lens. One who uses the same terminology that the industry does. I partner with platforms and brands as an independent, non-exclusive strategic advisor—meaning you can tap into FASTMaster Intelligence to pressure-test your roadmap without disrupting your existing agency relationships. Let's talk.