The Viewniverse Scorecard: How My 2020 Data Predicted the Streaming Contraction

In 2020, I mapped the Viewniverse and warned that porting linear habits to streaming would fail. Six years later, the data proves it: premium FAST is a reality, ad-free utopias are dead, and broadcast is just a funnel. Here is the scorecard, and the survival playbook for Bundle 2.0 in 2026.

In late 2020, at the height of the streaming boom, I wrote the Variety VIP+ special report VIP’s Guide to the Viewniverse. It was an ambitious attempt to quantify 242 TV networks and streaming services on a single scale to see who actually mattered. (Yes, I made media maps in 2020 before they were cool).

The data contained a punchline that executives didn't want to hear: YouTube and Netflix weren’t just winning; they had rewritten the psychological contract with the viewer.

While legacy media was busy porting linear habits into apps—forcing weekly releases, stuffing and expanding ad pods, and ignoring choice fatigue—the data showed the audience had already moved on. They wanted control, they hated friction, and they didn't care about your network heritage.

Six years later, the diagnosis was uncomfortable but correct. Here is the scorecard on what the Viewniverse predicted, what the industry learned the hard way, and why I’m launching the 2026 edition to measure what matters now.

1. The "Premium FAST" Prophecy

- The 2020 Call: "VIP predicts premium FAST channels within the next 2 years."

- The Verdict: Bullseye.

Back then, FAST was treated as a digital bargain bin for library content. I argued it was a structural escape valve. By 2026, PAST isn't an oxymoron; it’s a core retention strategy for AMC+, Disney+, Paramount+, Peacock and more. FAST mechanics have been swallowed whole by paid services, proving that subscribers don't always want to browse—sometimes, they want to be programmed to, crucially with a much smaller channel offering than traditional FAST. Lean-back viewing isn't a relic of cable; it's a feature of human psychology.

The Data: By mid-2024, Nielsen’s The Gauge revealed that Tubi and Pluto TV alone accounted for over 3% of total US TV viewing, outpacing several top-tier cable networks. In response to choice fatigue, major SVODs adapted—evidenced by Disney+ officially rolling out always-on, FAST-style channels (like ABC News Live and curated continuous streams) directly inside their premium app.

2. The Death of the Ad-Free Utopia

- The 2020 Call: "Business models are outdated... Audiences don't like to wait... Too many ads."

- The Verdict: Hit.

In 2020, SVOD wars were fought on a false binary: "ad-free premium" vs. "cluttered linear." Viewniverse data showed younger demos flocked to services with low or smart ad integration, not strictly no ads. The market conceded: HBO Max (2021), Netflix (2022), and Disney+ (2022) all rushed to launch ad tiers. The realization wasn't just that "ads exist," but that ad load is a product design problem. Recreate the 6-minute cable ad pod, and you die. Design a low-friction ad tier, and you build a funnel.

The Data: The shift was seismic. By mid-2024, Netflix announced its ad tier had surged past 40 million global monthly active users, accounting for 40% of all new sign-ups in ad-supported countries. Concurrently, Antenna reported that ad-supported tiers were driving the vast majority (nearly 60%) of all premium SVOD subscriber growth.

3. Broadcast’s New Job Description: The Front Door

- The 2020 Call: Broadcast networks had to "reinvent themselves online" because younger viewers were showing alarming detachment.

- The Verdict: Hit (with a twist).

The 2020 map showed a terrifying gap: older viewers were loyal to the network brand, while younger viewers were loyal to the show. Fast forward to today: Broadcast & Cable brands have become the "front door" for the streaming house (ABC/FX to Hulu; NBC/Bravo to Peacock; CBS/Comedy Central/Showtime to Paramount+). The TV network is no longer the final destination; it is a massive, wide-mouth funnel designed to push audiences into the digital ecosystem where the real ARPU lives.

The Data: While traditional broadcast TV’s share of viewing has steadily dropped toward the 20% mark (per Nielsen), broadcast IP is the engine of streaming engagement. Case in point: NBCUniversal's Suits broke all-time Nielsen streaming records with nearly 58 billion minutes viewed across Netflix and Peacock in a single year, proving linear heritage fuels digital dominance when placed on the right platform. Conversely, they also proved that the audience making legacy content relevant again is no longer on traditional TV with the abject failure of Suits: LA.

The failure wasn't just that it aired on legacy TV; the failure was prioritizing legacy TV for the first-window US release. To capture a digitally native audience, the SVOD that made the content relevant again cannot be treated as a secondary acquisition window after it airs somewhere else. It must be the primary destination.

4. Stop Copying Linear’s Homework

- The 2020 Call: Porting the "weekly release schedule" to streaming is a legacy habit, not a strategy.

- The Verdict: Nuanced Hit.

Netflix proved you didn't need weekly releases to create a hit. But the industry learned that some event programming demands it. The winners of the last five years didn't just dump content online; they designed release strategies (batches, drops, weekly events) that matched the job the content was hired to do.

The Data: Antenna data highlights the rise of "serial churners"—users who frequently cancel and restart subscriptions based on content drops. Platforms that successfully mix binge-drops (for library retention) with strategic weekly drops for cultural watercooler moments (like HBO's The Last of Us or FX/Hulu's Shogun) effectively manipulate the calendar to suppress this active churn rate.

The Ways to Grow Playbook: 2026 Edition

If you are a media brand trying to survive the next contraction, the Viewniverse logic still holds. Here is the consulting playbook I use when helping brands navigate this map:

- Dual Distribution is Mandatory: You need a Paid Tier for intimacy and ARPU, and a FAST/Ad-Tier for scale and habit. Force a binary choice, and you lose.

- Make PAST a Habit Layer: Use always-on streams inside your app to solve choice fatigue. If a user spends 10 minutes browsing and plays nothing, they churn. If they default to a PAST channel, they stay.

- Fix the Calendar: Erratic seasons kill streaming habits. If your franchise goes dark for 18 months, you don't have a franchise; you have a library title.

What Comes Next?

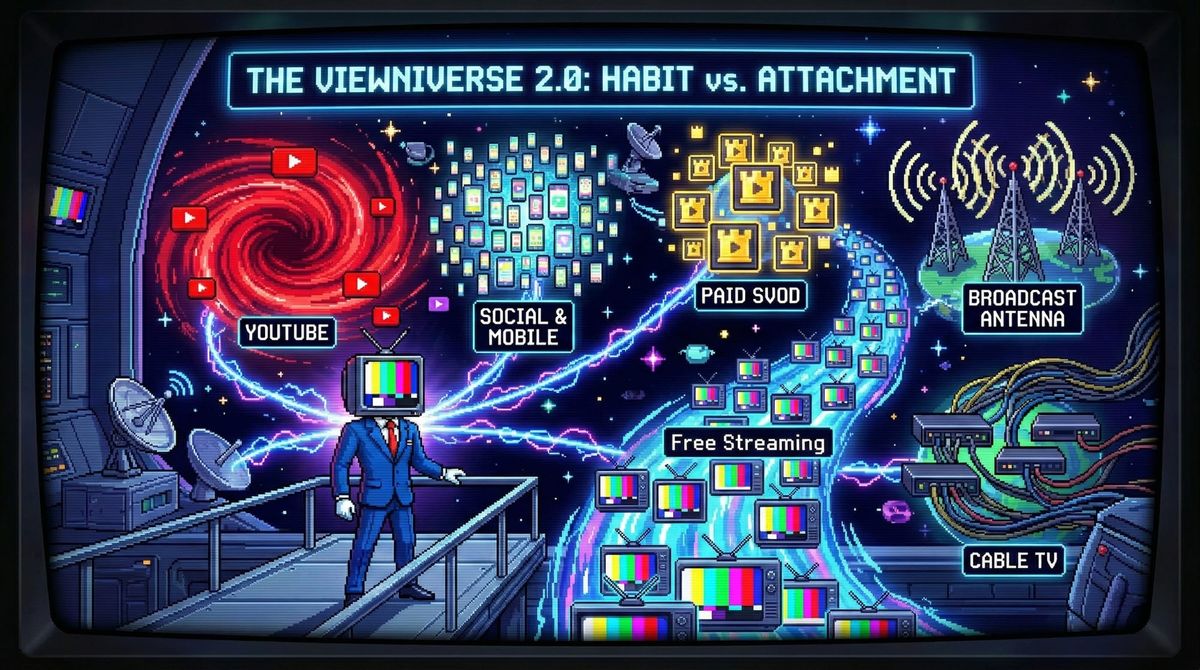

The 2020 Viewniverse measured Habit vs. Attachment. The 2026 Viewniverse needs to measure Choice vs. Inertia.

Welcome to "Bundle 2.0." Subscribers now have services they chose and services they inherited (via telco deals, Amazon channels, or aggregators). Understanding the difference between a subscriber who loves you and a subscriber who just hasn't canceled you yet is the next billion-dollar question.

Understanding the difference between a subscriber who chose you and a subscriber who inherited you is the next billion-dollar question. I am currently designing the field work for Viewniverse 2026. If your executive team needs to know where you actually stand on the map, let’s talk.